HOP Motor living FAQ/update page

As of 1 December 2021, we have updated our motor application to meet the new CCCFA requirements – however, there will continue to be ongoing updates to the application and process. This page will be updated as/when there are new pieces of information to share.

.

23/06/2022 – Matariki holiday hours

Please find listed below the hours that our Credit, Payouts and Dealer Support teams will be working over the upcoming holiday weekend.

Credit – No Change

- Friday 24 June (Matariki): 9.00am – 5.00pm

- Saturday 25 June: 9.00am – 5.00pm

- Sunday 26 June: 9.00am – 5.00pm

Phone: 0800 520808

Email: [email protected]

Payouts – Closed

Dealer Support – Closed

27/05/2022 – Introduction of ‘premium bypass’

(Please clear your Google Chrome cache if you’re not seeing these updates)

We have introduced a ‘premium bypass’ to allow certain customers to bypass BSR/OCR – whether a customer qualifies for the bypass will be determined by their credit and income/expense information.

If an application meets certain criteria, it will bypass the requirement for bank statement retrieval and be conditionally approved – you will then be notified by email. The status of the application will also reflect the outcome of the initial checks, as per the below.

| Conditioned | Conditionally approved, please proceed with the standard documents and proof of income. |

| Referred | Bypassed transactional history process but has flags which need reviewing before proceeding. |

| Conditioned Referred (Waiting for statements) | Did not pass bypass – follow existing process. |

Please note:

- Changing the application details of a non-bypassed application won’t change the bypass outcome

- Changing the application details of a bypassed application (e.g. adding on insurance) may cause the bypass to fail on affordability, and editing the application back to the original pass values will not currently allow the application to automatically re-bypass the step.

- If the customer wishes to proceed with the originally bypassed loan values, please contact the Heartland Credit team to discuss this process.

For us to implement this premium customer bypass, we also need to add additional suitability questions to Docman – all suitability questions in Docman will also now need to be completed before an application can be submitted in HOP.

Below is a breakdown of the two new processes.

Completing income and expense questions before submitting in HOP

1. Once you have finished filling out the application in HOP, click the Save button and then Save and Continue. If an application has been previously saved, click the ‘Update Application’ button.

2. Click the ‘Submit Application’ button which will bring up a pop-up.

3. Click the Open Document Manager link in the pop-up message.

4. Click the Income Verification tile and then the Start income and expenses questions

5. Complete all questions appropriately.

Note: You will only be able to add Buy Now Pay Later and Revolving Credit debts in Docman. If you make changes/additions to an auto-populated debt, this will need to be done through HOP using the Update Debt Values process.

1. Once all the questions on both pages have been completed, click Submit and return to HOP.

2. Close the pop-up and click the Submit Application button.

Updating debt values

Follow the below process in HOP if you notice that the auto-populated read-only debt value(s) are incorrect in Docman.

1. Go to the HOP view with all applications and click the application number.

2. Once the Application Details window pops up, click Edit.

3. Click on the Application and then Expenses tab at the top of the page.

4. If there are multiple applicants, confirm you are editing the correct one.

5. Update the value for the debt you need to edit or add an additional debt.

6. Click the Update Application button.

7. Click the Submit Application button.

Note: Once an application is submitted, you won’t be able to edit the debt values through HOP.

29/04/2022 – Changes to customer due diligence (CDD) forms due to new regulations

As you may be aware, a new set of anti-money laundering (AML) and countering financing of terrorism (CFT) regulations has come into full effect from 29 April 2022.

From this date onward, Heartland will need to understand whether newly onboarded companies and limited partnerships have a nominee director or general partner. We will ask company and limited partnership customers the following question and record their answer in the respective CDD checklist:

Does the company/limited partnership have any nominee director/general partner?

- If YES: Written confirmation will be required, including the name and date of birth of the individual, and enhanced due diligence (EDD), i.e. source of funds/wealth, will be conducted on the entity.

- If NO: No further action is required. Please note that no written confirmation is required from the customer.

Updated company and limited partnership checklists will be published in HOP with the additional question. For more details, please get in touch with your Relationship Manager.

13/04/22 – Updates to statuses, notifications and sending links

We’ve made some improvements that will make it easier and simpler for dealers to see how their customers’ applications are progressing, as well as improve turnaround times. Here is a breakdown of these changes.

1. You will see that the status ‘New – Waiting for Statements’ has now been replaced with two statuses clarifying whether the application is referred or conditioned, based on the outcome of the initial checks. The new statuses you will see are as follows.

- ‘Referred – Waiting for Statements’

- ‘Conditioned – Waiting for Statements’

2. You will now also receive an email notification once your customer’s application moves into one of the above new statuses to alert you of the application’s progress and outline next steps.

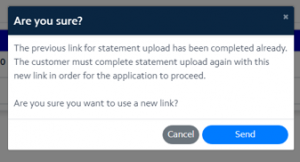

3. If you want to send your customer a new bank statement retrieval link, you’ll now only see a pop-up if your customer needs to recomplete bank statement retrieval (for example, if they forgot to include their credit card statements). The pop-up will confirm that the customer has already completed retrieval, and that if you send a new link they will need to complete it again using the new link.

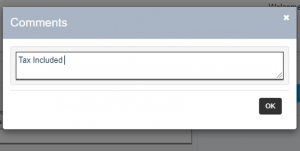

31/03/2022 – CO2 emissions fees charged from 1 April

As you’ll be aware, the new CO2 emissions fee comes into effect 1 April 2022. This fee will be charged on high emissions vehicles when they are first registered in New Zealand. The fee amount will depend on the amount of CO2 the vehicle emits and will need to be paid at the time the MR2A is processed.

Financing the fee

We will be able to finance the fee (subject to Credit approval) but we will require you add a note to your HOP application. In order to do this, please note “Tax included” in the comments field of your HOP application.

The Clean Car Discount (rebate)

From 1 April 2022, the Clean Car Discount, which is designed to make low emissions vehicles more affordable, offers rebates that are also based on the vehicle’s CO2 emissions. As the amount of the rebate will vary based on the vehicle, we recommend that you liaise with your customer to understand whether they want to consider applying the rebate to their loan as a balloon payment (for example a few weeks or months into the loan) – this allows time for the customer to process and receive the ‘rebate’.

If you any questions, please get in touch with your Relationship Manager.

11/03/2022 – Non-affordability related declines to be given earlier in application

As part of the application process, we need to run the information through our business rules. This step has now been brought forward in the process to sit before the suitability questions and income verification.

What does this mean?

This means that applications that fail on factors like credit score, age (under 18), bankruptcy, existing arrears etc. will now receive the decline before they are prompted to fill out the suitability questions or complete income verification, saving time and effort for both you and the customer.

This technical change will also allow us to give you more information about the status of your application earlier in the process, and you will see enhancements over the coming month to support this. For the meantime, declined applications will be decisioned earlier, and these applications will not need to go through the statement retrieval process.

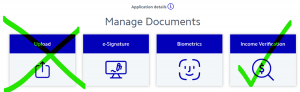

20/01/2022 – Removing ‘Send to Credit’ button from Upload section in Docman

Within the ‘Upload’ section of Docman, we have removed the button entitled ‘Send to Credit’. This button was originally created for dealers to send additional info (such as payslips) directly through to Credit.

However, with the recent CCCFA changes to our application process, there has been some confusion around whether to use this ‘Send to Credit’ button to send customer bank statements through.

In order to remove this confusion, we’ve removed the button – bank statements must be provided via the ‘Income verification’ tab, and any other docs (like payslips) that Credit asks for can be emailed directly through to the team.

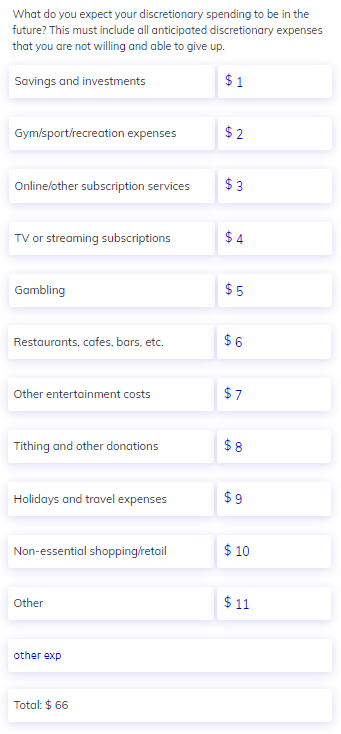

16/12/2021 – New suitability question around discretionary spending

Thank you again for working with us as we ‘bed’ the new CCCFA rules into the application process. One part of the process that we’re looking to streamline is around a customer’s discretionary spending, which may change month-to-month depending on their situation.

It’s important for us to understand what a customer’s discretionary spending will be in the future so we can evaluate whether they’d be able to afford their loan repayments. For us to have the right information on-hand to assess affordability, we’ve decided to add an additional mandatory suitability question in Docman to help us identify the customer’s future discretionary spending up front.

Here is how the new question will look. All discretionary expenses fields must be completed, even if the answer is $0.

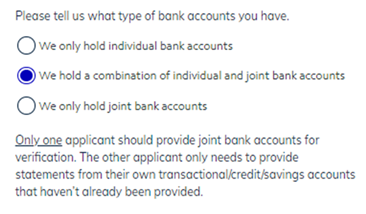

Reminder: joint accounts should only be submitted once

We’ve added a reminder in the suitability questions section of Docman that any joint statements should only be provided once – if two applicants hold a combination of joint and individual bank accounts, one applicant should provide Heartland with all their own accounts (joint and individual) and the other applicant only needs to provide their individual accounts.

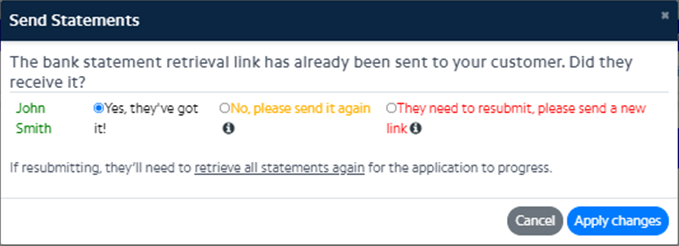

8/12/2021 – Updated instructions in pop-up

We have made an update to the ‘send statements’ pop-up in the Income verification tab. It will now ask whether the customer has received the bank statement retrieval link.

- If they’ve received it, no further action is needed. Please click ‘Yes, they’ve got it!’ and ask your customer to click the link in the email already sent. This will progress their application.

- If they haven’t received the original link and completed retrieval yet, you can send the link again. Please click ‘No, please send it again’ and your customer will receive the link in their email inbox automatically. It doesn’t matter whether they click on this new link or find the old one in their inbox, as long as they complete retrieval using one of the links.

- If you are resubmitting your customer’s application AND they need to retrieve statements again (this might be because they have forgotten a statement the first time) please click ‘They need to resubmit’, which will send them a new link. The customer must click this new link to re-retrieve all their statements – they should not use the old link again.

7/12/2021 – Common questions and friendly reminders

We’ve learnt a lot since go-live last week, and we wanted to share some answers to common questions we’ve been asked which may be helpful to you:

No – please make sure you only upload income via the Income Verification tile, not through the Upload tile – the Upload tile is where you send your completed paperwork to us for payout.